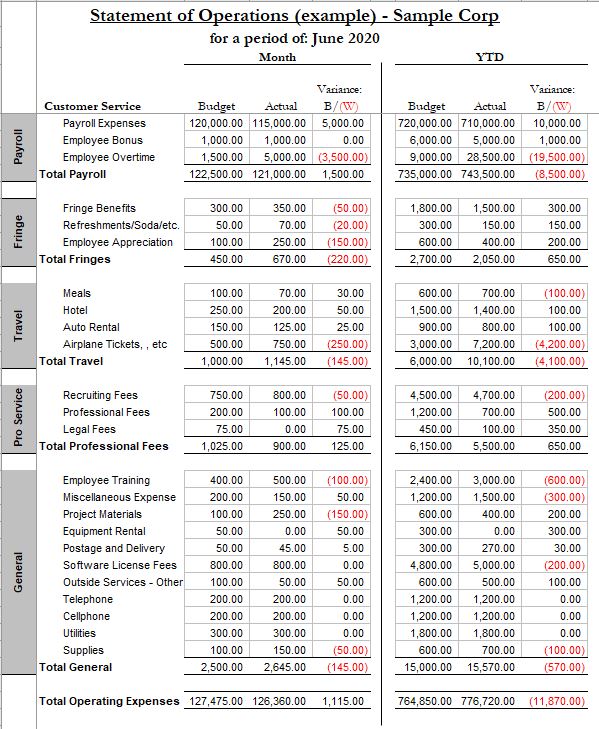

Statement of Operations Budget - Free Excel Download

This example budget shows the different types of expenses, presented by finance, that have been determined by you and upper management along with the associated costs that your department has incurred. Generally, an operating expense budget will have the current months and year-to-date (YTD) budgeted and actual expenses along with the variance. The cells with parentheses means you went over budget. It is also highlighted in red. As you can see, this is an expense report for the month of June with YTD data, which in this case is six months worth of expenditures. Here is the breakdown:

- As far as payroll, you are under budget regarding the amount of staff you have allocated to your department, but you are way over on overtime. This has caused you to go over budget by $8,500 YTD. This clearly shows you better get on the ball and start hiring, or investigate on whether or not you have a process issue that is causing you to require so much overtime.

- As for fringe benefits, you went over for June, but still within your YTD budget, so there is not too much concern here.

- As for travel, you are over budget mostly because of higher than expected flight costs. You need to see if these trips are truly needed, and if so, try to book sooner to reduce costs.

- As for professional services, you are over on recruiting fees but under for legal or other professional fees. Chances are you do not need as much allocated to you for legal and you might want to adjust for next years budget.

- As for general expenses, you are over on training and should re-adjust to a more accurate cost for next years budget, due to the importance of training. You also need to re-adjust the needed software licenses for your hosted database solution. These both could have been mistakes at the time of creating the budget, which makes you look bad.

- Most other expenses are in check.

Overall for the month of June, you were under budget by a respectable amount, which is a good thing. However, YTD, you are over $11,870. This trend shows you will be at least $23,000 over budget by years end. This is not good. The two issues that stand out the most are overtime and flight costs. You would need to start reducing these costs right away. By also reducing the other not-so-significant costs, you might be able to get back to budget as every little bit counts. This is just an example, and hopefully you would not have ever let it get to this point. By looking at the monthly and YTD numbers, you will always know exactly where you stand.

It is your job to justify the needed requirements, such as the staff needed along with the different monetary levels associated with each staff member. However, you also need to work with upper management and understand where they are coming from if you cannot get what you requested. Sometimes, there is just not enough money in the budget to accommodate all of your requests.

The way you set up your department should help greatly in justifying certain requests, such as raises based on skill levels, materials to streamline process, and trending data that shows the need for more staff throughout the year. This will also help if you are asked to reduce head count in the new years budget. You will be able to make the most efficient cuts with the least harm to the department, while still being able to show the possible ramifications of the cuts such as less after hours coverage, which might reflect on customer survey reports and affect goals.

There is also the domino effect with a product related business where you can cut costs during projected slow sales. You should not have overtime due to fewer products, which in turn means less costs of materials, which in turn means less shipping and receiving costs, etc. For example, if you are overstocked, and costs are high while sales are low, as was anticipated, then you did not do your forecasting and cut production correctly. The bottom line is you need to be able to determine, and help adapt, to the priorities, trade-offs and needs to the business in order to make budget and stay profitable.

Setting up a Budget for your Department - Statement of Operations - Capex

You as manager need to fully understand your role in the budgetary process. It is the most basic financial planning and control tool. Every manager needs to know what costs are associated with their department, and how in relation are they doing to that budget. You might achieve your departmental goals, but if you go over budget in order to achieve those goals, you create financial problems for the company and jeopardize your own job performance review. In most cases, part of your performance appraisal will be based on whether or not you were within budget for the year.

Budgets need to be realistic. You can’t just say at a whim you need 20 new people, just as upper management can’t say you have only $10 for a years worth of training classes. Budgets are used to investigate variances, whether you went over or under budget, and address the reasons for the variances. You need to always look at ways to control those variances by controlling costs. By being on top of your budget, you might be able to make changes before it’s too late and you end up having to reduce staff or eliminate a branch of your department.

Great managers always look at significant expenses they can reduce or eliminate, such as overtime, travel and entertainment. Also keep in mind, just because you created a budget for the year, it can change if sales are bad or below target. You might have the budget to hire someone, but it can be eliminated if sales do not improve, thus a hiring freeze. You might also have an employee who quits and you cannot replace them, which is known as attrition. You will during your managerial career have to deal with ways of cutting costs, including layoffs. On the other hand you might be able to increase your previously budgeted staff if sales are better than expected.

There are basically two types of budgets, a capital expenditure budget and operating budget:

- Capital expenditure (also known as “Capex”) relates to costs associated with plant and equipment. This is equipment that generally lasts for more than a year such as a copy machine.

- Operating budget, which is related to the normal day-to-day operations and expenditures such as payroll, supplies, and miscellaneous. There are two types of budgets within an operating budget, sales budgets and expense budgets:

- Sales budget is associated with comparison and variance of the actual revenue brought with the projected revenue.

- Expense budget applies to all areas incurring operating expenses, including the sales department. This is the budget we will focus on.

Lets look at a budget as if you are the “Customer Service Manager” in which you would mostly work with finance on budgetary items like staffing (payroll), training expenses, software licenses needed, and general expenses. You would need to make sure that you have your staffing goals and needs figured out and stick to them as close as possible. You should really look over the budget carefully with finance; due to sometimes items might be in your bucket that you feel belong to another department. Finances job is to make sure everyone submits their required operational expenses and then compiles those numbers for upper management in a way that makes sense. Finance acts as a middleman between department heads and upper-management when it comes to budgets. It is not their job to decide on what you need. They have been given a monetary amount from upper management and should help you allocate to your needs.

| ||||